All Categories

Featured

Table of Contents

Life insurance policy covers the insured individual's life. If you pass away while your plan is energetic, your beneficiaries can utilize the payment to cover whatever they select clinical costs, funeral expenses, education, lendings, everyday prices, and also financial savings. If you have a plan, conduct routine life insurance coverage assesses to see to it your beneficiaries are up to date and recognize how to assert life insurance policy coverage if you pass.

Depending on the problem, it may influence the plan type, price, and insurance coverage amount an insurance firm offers you. Life insurance policy plans can be categorized right into three main teams, based on how they function:.

Who provides the best Cash Value Plans?

OGB supplies 2 fully-insured life insurance policy plans for staff members and senior citizens with. The state shares of the life insurance policy premium for covered workers and retirees. The 2 plans of life insurance policy available, along with the matching amounts of reliant life insurance used under each plan, are noted below.

Term Life insurance policy is a pure transference of threat for the payment of premium. Prudential, and prior service providers, have been giving insurance coverage and assuming threat for the settlement of premium. In case a covered person were to pass, Prudential would recognize their obligation/contract and pay the benefit.

Plan participants currently registered who desire to add dependent life coverage for a spouse can do so by giving proof of insurability. Staff member pays 100 percent of dependent life premiums.

Agreement Collection: 83500. 2018 Prudential Financial, Inc. and its related entities. Prudential, the Prudential logo design, the Rock sign, and Bring Your Challenges are service marks of Prudential Financial, Inc. and its relevant entities, signed up in many territories worldwide. 1013266-00001-00.

Who has the best customer service for Senior Protection?

The rate framework allows employees, spouses and cohabitants to pay for their insurance coverage based upon their ages and chosen protection quantity(s). The maximum ensured issuance quantity readily available within 60 days of your hire day, without proof of insurability is 5 times your base yearly wage or $1,000,000, whichever is less.

While every effort has been made to make certain the accuracy of this Recap, in the occasion of any inconsistency the Summary Plan Summary and Strategy Document will certainly dominate.

What happens when the unexpected comes at you while you're still to life? Unforeseen ailments, lasting handicaps, and much more can strike without warning and you'll wish to prepare. You'll wish to see to it you have alternatives readily available simply in case. Thankfully for you, a lot of life insurance policy policies with living benefits can provide you with monetary aid while you live, when you require it the a lot of.

, yet the advantages that come with it are component of the reason for this. You can add living advantages to these strategies, and they have money worth growth possibility over time, indicating you might have a few different choices to make use of in situation you require moneying while you're still alive.

Why do I need Death Benefits?

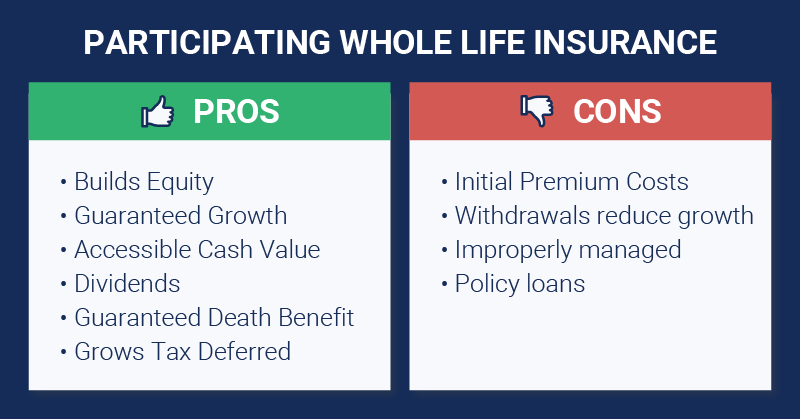

These plans may permit you to add specific living benefits while additionally permitting your strategy to build up cash worth that you can withdraw and use when you require to. resembles whole life insurance coverage in that it's an irreversible life insurance coverage policy that means you can be covered for the remainder of your life while appreciating a plan with living advantages.

When you pay your premiums for these plans, part of the settlement is drawn away to the cash money worth. This cash money worth can grow at either a dealt with or variable rate as time proceeds depending on the sort of policy you have. It's this amount that you may have the ability to access in times of demand while you live.

However, they'll accrue interest charges that can be damaging to your survivor benefit. Withdrawals let you withdraw money from the cash worth you have actually collected without rate of interest charges. The drawback to using a withdrawal is that it can increase your premium or reduced your death advantage. Surrendering a plan essentially means you have actually ended your plan outright, and it immediately offers you the cash worth that had accrued, less any abandonment charges and outstanding policy costs.

Using cash money value to pay costs is basically just what it seems like. Depending upon the kind of policy, you can make use of the money value that you have actually accumulated with your life insurance policy policy to pay a section or all your costs. A living advantage cyclist is a sort of life insurance policy motorcyclist that you can include in your life insurance plan to make use of in your life time.

Who offers Term Life Insurance?

The terms and amount offered will be defined in the plan. Any living benefit paid from the survivor benefit will certainly lower the quantity payable to your recipient (Guaranteed benefits). This payment is indicated to aid supply you with convenience for completion of your life as well as assist with medical costs

Crucial disease motorcyclist makes certain that advantages are paid directly to you to pay for therapy services for the ailment defined in your policy contract. Long-lasting care motorcyclists are implemented to cover the cost of in-home treatment or retirement home expenditures as you obtain older. A life settlement is the process whereby you market a life insurance policy plan to a 3rd party for a round figure repayment.

How long does Premium Plans coverage last?

That depends. If you're in a permanent life insurance coverage plan, then you have the ability to take out cash money while you live via financings, withdrawals, or surrendering the plan. Before making a decision to tap right into your life insurance policy plan for money, seek advice from an insurance coverage agent or rep to establish how it will affect your beneficiaries after your fatality.

All life insurance policy plans have something in common they're made to pay money to "called recipients" when you pass away. Trust planning. The beneficiaries can be several individuals or perhaps an organization. For the most part, plans are acquired by the individual whose life is insured. Nevertheless, life insurance policy plans can be gotten by spouses or any person who is able to prove they have an insurable passion in the person.

Why is Flexible Premiums important?

The policy pays cash to the called recipients if the insured passes away during the term. Term life insurance policy is planned to supply lower-cost coverage for a specific period, like a 10 year or 20-year period. Term life policies may consist of an arrangement that allows coverage to proceed (renew) at the end of the term, even if your health condition has altered.

Ask what the costs will be prior to you renew. Ask if you lose the right to renew at a specific age. If the plan is non-renewable you will certainly need to look for protection at the end of the term. is different since you can maintain it for as long as you require it.

{kind=link}

Latest Posts

Final Expense Insurance Canada

United Burial Insurance

How To Sell Final Expense Insurance